Research Platform

BAQLABS is our realistic research stack.

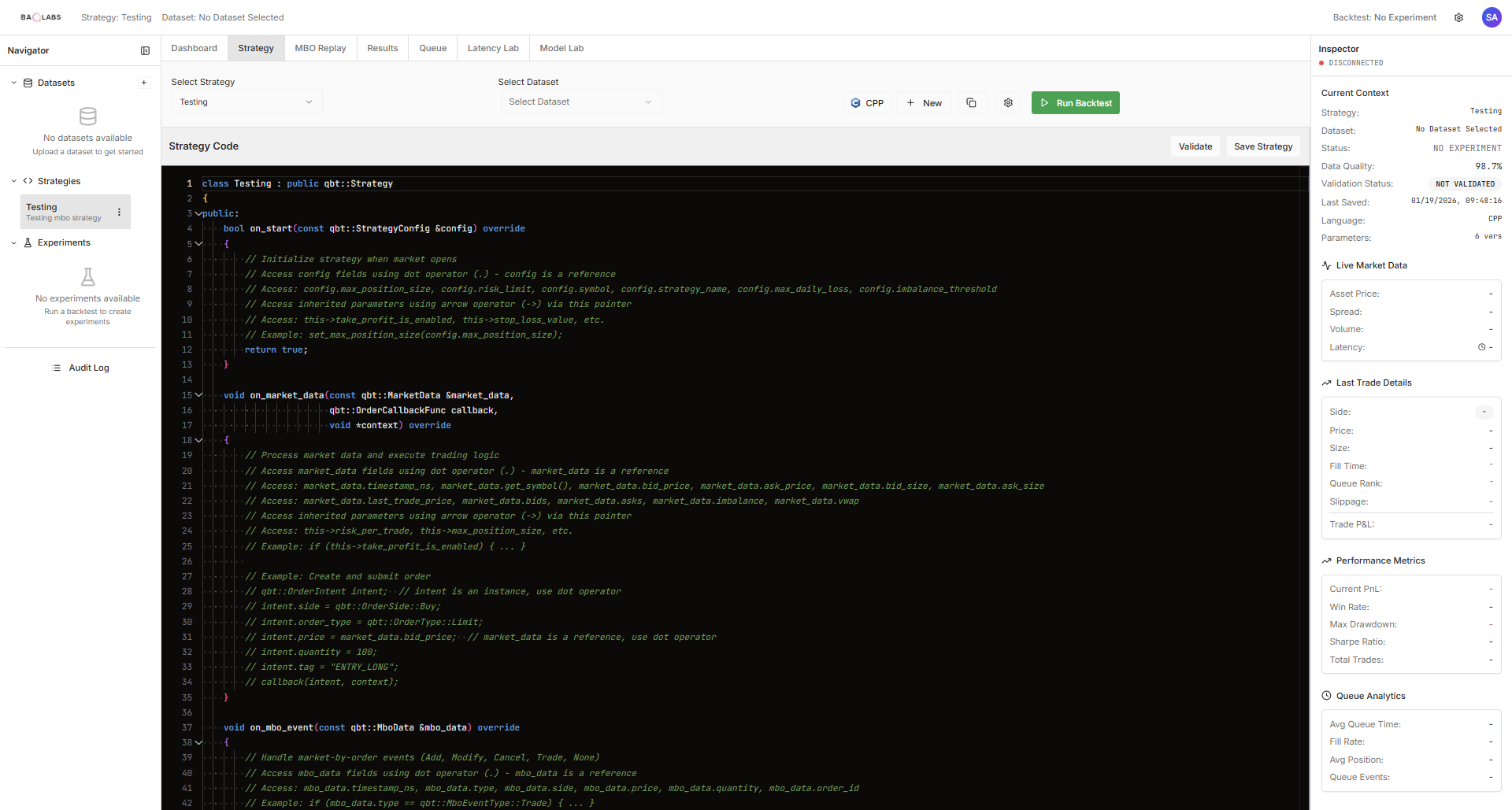

A Institutional grade environment for validating strategies under market microstructure constraints that is built to reduce the gap between backtest and live deployment.

Queue-aware simulation

Latency controls

Order book analytics

C++ / TypeScript

Strategy Builder

www.baqlabs.comMBO replay · Queue analytics · Latency Lab · Model Lab · Results